The COVID-19 pandemic’s devastating impact on the job market has left many households unable to pay their mortgages or rents. Fortunately, the speedy intervention provided by the CARES Act ensured mortgage forbearance options for homeowners who were financially harmed by the pandemic.

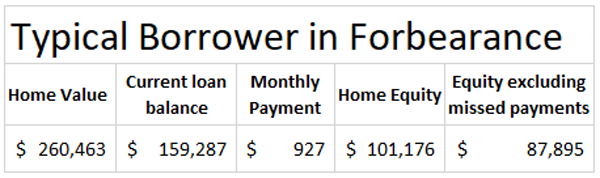

A typical homeowner in forbearance appears to have sizeable equity in their home, with median equity just over $100,000 and loan to value ratio[2] at about 61%. Even after accounting for missed mortgage payments, a typical homeowner in a forbearance is estimated to have about $88,000 in equity — which is generally more than enough to cover the costs of selling a home and still have some equity left over.

There are still over 2 million borrowers in forbearance with about half of them at least 180 days behind on their mortgage payments. Among borrowers in forbearance, 2.9% are still in negative equity, or about 58,000 loans.