Remember when housing prices Nationwide started falling in 2007 and bottomed out in 2011? The period in history was known as The Great Recession.

The term “housing bubble” summed up that miserable period. The bubble was created by speculation and fueled by easy mortgage money.

Let’s compare some key factors of the Great Recession to today’s environment.

In 2006 the demand was driven by speculation. Today it’s driven by end users.

When the bubble burst in 2006 we had a 20-month supply of homes for sale. Today we have a 2-month supply.

New home construction was way up in 2006… today builders can’t build fast enough to keep up with demand. With the cost of construction increasing, it’s likely supply won’t catch up with demand anytime soon.

In 2006 a 30-year fixed rate loan was 6%. Today it’s 3%.

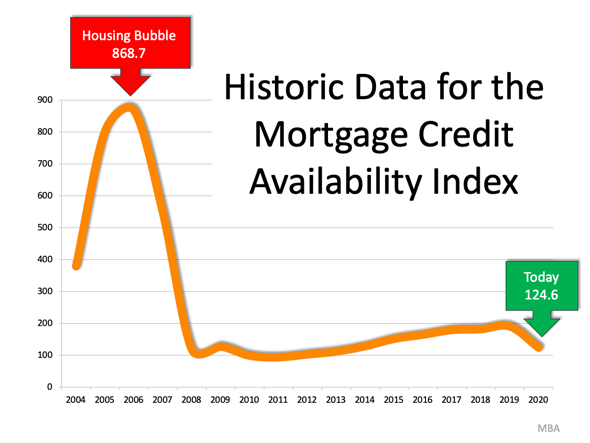

But here’s the really significant piece of data. Take a look at this graph.

You can see It was pretty loose in 2006. But by 2008 everything changed. It dropped like a Double Black Diamond ski slope. It’s been remained flat at that level for the last 12 years. The bottom line is that people who have mortgages on their homes now are much better qualified and those loans are very well underwritten.

But what about all the potential foreclosures once Federal moratoriums are lifted?

Consider this. According to the Mortgage Bankers Association, 62% of all US homes have a mortgage. Taken together, EQUITY for those mortgaged properties surged to more than $1.5 trillion. That’s an increase of more than 16.2% from a year earlier.

It’s hard to say how many of the remaining borrowers in forbearance have either experienced a real hardship or are just taking advantage of the fact they haven’t had to make a mortgage payment for the last 12 months.